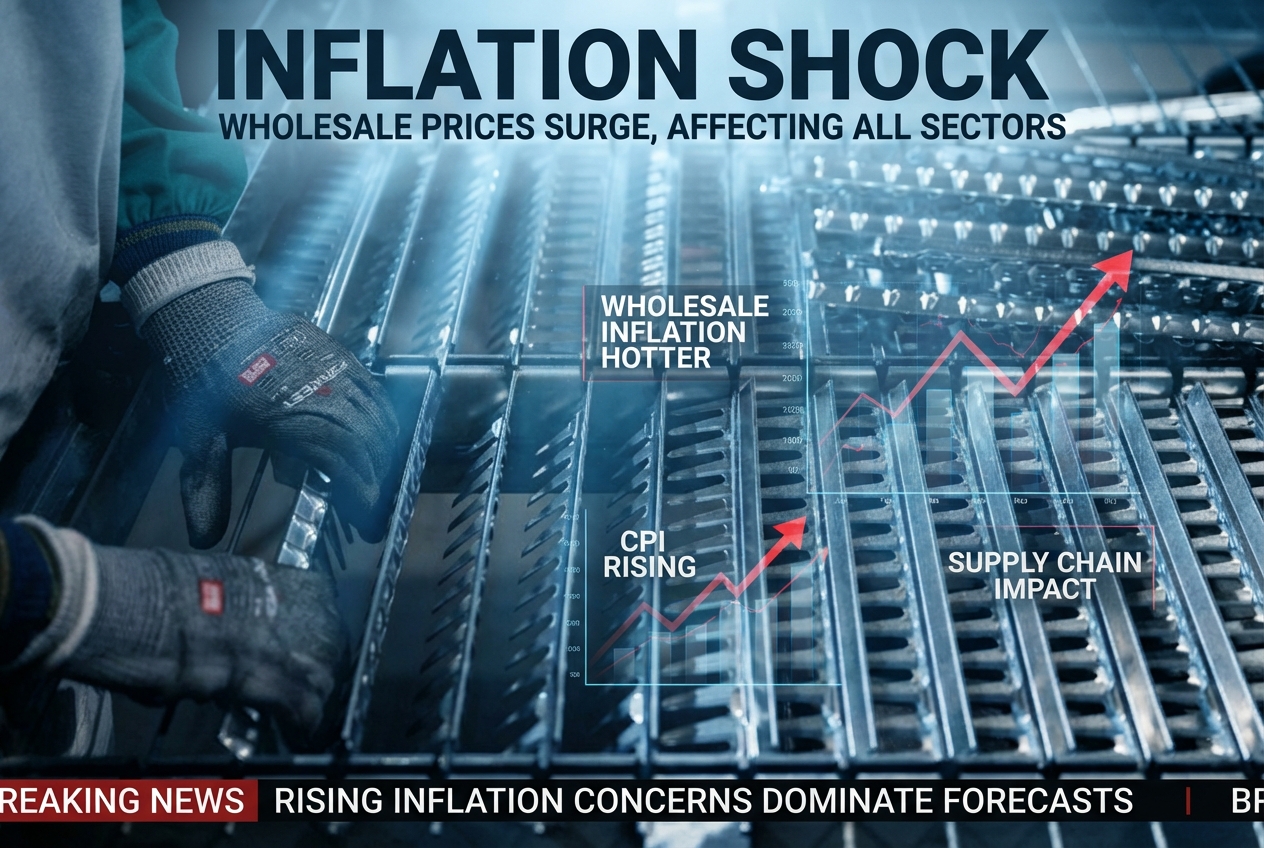

The whispers in the financial corridors have turned into a clear, loud alarm bell. Rising inflation concerns have dominated economic forecasts globally, but this week’s data delivers a sharp, targeted punch to US market sentiment. Wholesale inflation, the often-ignored precursor to your own household budget pain, came in significantly hotter than anticipated for January. This isn’t just statistical noise; it’s a flashing signal that the hidden tax of tariffs is now actively translating into higher prices for the goods and services Americans buy every day. Wall Street reacted instantly, fearing the Federal Reserve’s timeline for interest rate relief has just been dramatically extended.

The core issue lies in the latest figures from the Bureau of Labor Statistics detailing the Producer price index. Economists pegged the monthly rise for the wholesale metric at a moderate 0.3 percent, anticipating the annual rate to settle around 2.6 percent. The reality? The PPI clocked in at a robust 0.5 percent rise month-over-month, pushing the annual rate up to 2.9 percent. This overshoot isn’t minor; it represents a decisive move away from the much-hoped-for disinflationary glide path. Stock markets, perpetually sensitive to Federal Reserve policy tied to inflation metrics, tumbled swiftly on the news. The Dow shed over 700 points, demonstrating a palpable fear that sticky wholesale costs will prevent the Fed from pivoting to rate cuts anytime soon.

The Hidden Hand of Tariffs in Trade Services

To understand the depth of this inflation shock, one must look beyond simple goods pricing and examine the structure of the wholesale index. While volatile categories like gas and food saw decreases last month, masking some underlying pressures, the true culprit emerged in the “trade services” category. This segment, which essentially measures the profit margins and markups absorbed by wholesalers and retailers as they move goods along the supply chain, skyrocketed by a concerning 2.5 percent. This isn’t raw material cost; this is the professional price tag being applied to the logistics and distribution of goods, and experts are connecting the dots directly to recent trade actions.

Michael Reid, a US economist at RBS Capital Markets, articulated the primary worry: tariffs are no longer being absorbed; they are aggressively being passed through. For months, analysts hypothesized about a time lag as businesses dipped into stockpiles of pre-tariffed inventory. That buffer period appears to be over. The sharp spike in trade services strongly suggests that tariffs imposed months ago are finally realizing their full economic impact as they migrate across multiple tiers of the supply chain. When a wholesaler marks up their services by 2.5 percent, that cost trickles down, compounding as it moves toward the final retail shelf.

Industries showing the most aggressive price increases in this trade services bracket include essentials and frequent purchases: apparel, footwear, chemical products, and crucially, health, beauty, and optical goods. These are not abstract industrial inputs; these are the items consumers purchase directly or indirectly every week. The implications are clear: the latest round of wholesale price increases are fundamentally tied to consumer-facing goods, meaning the consumer price index lurking ahead is likely to face similar, if not worse, upward pressure.

Core PPI Rockets to 10-Month Highs

Beyond the headline number, the core Producer price index reading—which strips out the often-volatile food and energy sectors to reveal the underlying inflationary trend—sent an even more chilling message to central bankers. The core PPI picked up sharply, rising 0.8 percent compared to December’s 0.6 percent reading. Annually, this metric surged to a 3.6 percent rate, marking its highest level in ten months. When food and fuel are removed, the underlying inflation story becomes starkly apparent: businesses are still facing persistent, structural cost increases that have nothing to do with weekly commodity fluctuations.

Furthermore, the report provided damning evidence against the current trade policy’s effect on finished consumer goods. Prices for finished consumer goods, excluding food and energy, escalated to an annual rate of 3.4 percent. This figure is the highest year-over-year inflation rate for this critical category in more than two years, specifically since the pandemic-era inflationary burst began receding. This corroborates the theory that the tariff structure, even with judicial challenges like the Supreme Court rulings on authority, is functionally driving up costs for imported finished products that U.S. businesses need to sell to maintain profitability.

It is vital to consider the alternative scenario presented by economists watching these margins. If businesses cannot pass these higher wholesale costs along to consumers—perhaps due to market saturation or competitive pressures—they face severe margin compression. While keeping consumer prices flat sounds appealing, the consequence is often delayed but equally damaging: reduced profitability leads directly to slower investment, hiring freezes, or worse, significant layoffs across affected industries. Therefore, this inflation spike presents the Fed with an impossible choice: either tolerate higher consumer prices or risk undermining the labor market recovery.

Historical Echoes: Tariff Inflation vs. Pandemic Inflation

The current situation carries unsettling echoes of the post-pandemic inflation shock, yet the mechanism driving it is fundamentally different. During the pandemic peak, inflation was fueled by overwhelming demand meeting severely constrained supply chains, amplified by massive fiscal stimulus. We saw widespread shortages and bidding wars for everything from lumber to used cars. The current environment is characterized by supply constraints imposed not by nature or accident, but by deliberate policy—specifically, tariffs creating artificial friction in global trade flows.

During the peak inflation of 2021 and 2022, the Federal Reserve was dealing with macroeconomic forces unleashed by global events. Their tools, primarily interest rate adjustments, were aimed at cooling demand. In contrast, the current inflation driver is largely supply-side specific, initiated by trade policy. Raising rates to combat tariff-induced pricing pressure is akin to using a fire hose to spray a leaky faucet. It slows overall economic activity—damaging legitimate growth sectors—while only indirectly addressing the specific, targeted cost pressures emanating from import duties.

This difference matters profoundly for market interpretation. Past inflationary scares allowed the Fed a relatively clear narrative: tighten until demand cools. Today, if they hold rates high to combat tariff inflation, they risk suffocating sectors that are otherwise healthy, leading to stagflationary outcomes where growth stalls but prices stubbornly refuse to fall because the underlying policy cause remains in place. The anticipation of this policy dilemma is precisely what drove the sharp downturn across equity indices immediately following the PPI release.

The Policy Conundrum: Fed Pause or Aggressive Tightening?

The immediate financial fallout centers on the perceived shift in the Federal Reserve’s calculus. Policymakers have often signaled that they need to see compelling evidence that inflation is sustainably trending toward their two percent target before initiating the long-awaited rate-cutting cycle. A hotter-than-expected January PPI suggests that the disinflationary trend, if it existed at all, has stalled or reversed at the wholesale level. This report hands the Fed a significant justification to maintain a “higher for longer” interest rate stance.

If the Fed prioritizes the inflation fight above all else, they must signal a delayed start to rate cuts. This has severe ramifications. Higher borrowing costs remain in place for consumers—think mortgages, auto loans, and credit card rates—which tightens household finances and slows consumer spending, the backbone of the U.S. economy. For businesses, it means increased debt service costs, directly counteracting any temporary margin relief they might have secured through inventory burn-down.

However, many economists point out that the services side of the equation, once trade-related margins are isolated, shows stability. This suggests that domestic demand for services is indeed cooling. The Fed’s challenge is to differentiate between inflationary noise caused by specific policy decisions and genuine aggregate demand overheating. Ignoring the tariff element and slamming the brakes on rate cuts based solely on the PPI overshoot might cause unnecessary economic contraction in areas of the economy that are not currently inflation-driven.

Future Scenario One: The Tariff Drag Continues

In the first possible evolution, the current trend solidifies: tariffs continue to exert sustained upward pressure on wholesale prices, and trade services inflation remains sticky or accelerates. This scenario forces the Fed into a defensive posture. Rates stay elevated well into the summer, potentially restricting the economy to near-zero growth territory simply to keep imported goods prices somewhat manageable for consumers. Businesses that rely heavily on international supply chains will struggle to maintain profitability without passing costs, leading to incremental price hikes across stores nationwide. This prolonged period of high rates and uneven inflation creates an environment ripe for market volatility, as investors constantly reassess margin risk versus recession risk.

The psychological impact here is significant. Consumers, having braced for relief, will experience renewed inflationary fatigue. This might manifest as an increase in precautionary savings and a sharp curtailment of discretionary spending, creating a self-fulfilling prophecy of economic slowdown despite the underlying policy causes being external to demand.

Future Scenario Two: Inventory Reversal and Price Correction

An alternative path hinges on the notion that businesses are still slightly overcompensating for expected future trade volatility. If supply chain managers eventually decide that the current environment is purely transitional—perhaps anticipating a shift in trade negotiations or political outcomes—they might choose to stop aggressively marking up their trade service margins. This leads to a scenario where the core Producer price index moderates quickly over the next quarter as companies decide absorbing smaller margins is preferable to risking consumer backlash or losing market share.

In this optimistic outcome, the Fed, seeing the core inflation metric drop rapidly without requiring deep interest rate cuts, can deploy modest rate relief. This scenario allows the Fed to claim success in engineering a soft landing—taming inflation without triggering a major downturn. However, this relies heavily on external policy variables shifting or businesses making a deliberate, costly decision to compress their own profits for the greater economic good, which history suggests is a fragile bet.

Future Scenario Three: Stagflationary Policy Trade-off

The darkest possibility integrates the worst aspects of the first two scenarios amplified by policy inertia. If the Fed refuses to cut rates, citing the persistent PPI, while the trade policies continue to actively choke off price relief on the supply side, the economy enters a period of genuine stagflation. Prices remain elevated due to structural tariffs and margin loading, but economic expansion grinds to a halt because borrowing costs are prohibitive. This combination is the nightmare for central bankers: stagnant economic output coupled with sticky, policy-resistant inflation.

Businesses facing both high input costs from duties and high financing costs for working capital will be forced to reduce headcount significantly. This scenario shifts the pain from the balance sheet to the employment statistics. The data suggests we are currently positioned precariously between Scenario One and Scenario Three, demanding extreme prudence from policymakers who must now navigate a supply-side inflation spike driven by legislative action, rather than just an excess of consumer demand.

FAQ

What specific economic metric signaled the wholesale inflation surge in January?

The key metric signaling the surge was the Producer Price Index (PPI), which measures wholesale inflation. It came in significantly hotter than economists had anticipated for the month.

How did the actual Producer Price Index (PPI) for January deviate from economist expectations?

Economists expected a moderate 0.3% monthly rise in the PPI, anticipating an annual rate near 2.6%. The actual results clocked in at a robust 0.5% month-over-month, pushing the annual rate up to 2.9%.

What immediate impact did the hotter-than-expected PPI news have on the stock markets?

Wall Street reacted swiftly, with the Dow shedding over 700 points immediately following the announcement. This illustrated palpable fear that the Federal Reserve’s interest rate cut timeline would be dramatically extended.

What component of the wholesale index is experts directly linking to the impact of recent tariffs?

The ‘trade services’ category within the PPI showed a massive 2.5% spike, which experts link directly to recent trade actions. This represents the markup applied by wholesalers and retailers in moving goods through the supply chain.

Why is the sharp rise in ‘trade services’ inflation more concerning than increases in raw material costs?

Trade services inflation reflects professional markups applied to logistics and distribution, suggesting that tariffs absorbed by businesses months ago are finally being passed on. This cost compounds across various supply chain tiers before reaching the consumer.

Which consumer-facing industries are showing aggressive price increases due to the trade services spike?

Industries showing aggressive increases include apparel, footwear, chemical products, and health, beauty, and optical goods. These are essential, frequent purchases, suggesting upcoming pressure directly on the Consumer Price Index (CPI).

What did the core Producer Price Index (PPI) reveal about underlying inflationary trends?

The core PPI, which excludes volatile food and energy, surged to a 3.6% annual rate, marking a ten-month high. This indicates underlying, structural cost increases facing businesses independent of commodity fluctuations.

What does a risk of severe margin compression imply for the economy if businesses cannot pass on wholesale costs?

If businesses cannot pass on costs, they face reduced profitability, which historically leads to slower non-essential investment, hiring freezes, or potential layoffs. This presents the Fed with a difficult trade-off between inflation control and labor market health.

How does the mechanism driving current inflation differ from the post-pandemic inflation shock?

Pandemic inflation was driven by overwhelming demand meeting supply constraints; the current inflation is largely driven by artificial, supply-side constraints imposed by deliberate trade policy (tariffs).

Why is raising interest rates considered an inefficient tool to combat tariff-induced inflation?

Hiking rates is designed to cool aggregate demand, but applying it to supply-side tariff friction is like using a fire hose on a leaky faucet. It risks suffocating healthy growth sectors without directly removing the input cost pressure from duties.

What are the ramifications for household finances if the Fed adopts a ‘higher for longer’ rate stance?

A sustained ‘higher for longer’ stance keeps borrowing costs high for consumer loans like mortgages and auto loans. This tightens household finances and risks slowing the consumer spending that drives the U.S. economy.

What data point suggests that domestic demand for services might still be cooling?

Much of the inflation appears concentrated in trade-related margins, while the stability in the overall services side of the equation suggests that domestic demand for services remains relatively temperate. This complicates the Fed’s inflation diagnosis.

In Scenario One (The Tariff Drag Continues), how is economic growth potentially affected?

Sustained upward pressure from tariffs forces the Fed to keep rates elevated well into the summer. This restrictive environment could push the economy toward near-zero growth as businesses and consumers pull back spending.

What consumer behavior might emerge if inflationary fatigue returns due to prolonged high prices (Scenario One)?

Consumers may increase precautionary savings and sharply curtail discretionary spending. This can become a self-fulfilling economic slowdown despite the underlying tariff-related cause.

What factor must materialize for the optimistic Scenario Two (Inventory Reversal) to take hold?

This scenario requires supply chain managers to decide the current trading environment is transitional and intentionally choose to absorb smaller profit margins. This bet hinges on businesses prioritizing market share over immediate profit protection.

If Scenario Two occurs, how might the Federal Reserve respond regarding interest rates?

If the core PPI moderates quickly due to margin compression, the Fed might deploy modest rate relief sooner. This allows them to claim success in engineering a soft landing without triggering a major recessionary contraction.

What defines the ‘stagflationary policy trade-off’ described in Future Scenario Three?

Stagflation occurs when the Fed maintains high borrowing costs to fight persistent PPI inflation, while the tariffs continue to keep supply costs high, resulting in stagnant economic output alongside sticky prices.

Which sector faces the highest risk of significant headcount reductions under the stagflationary outcome (Scenario Three)?

Businesses heavily reliant on international supply chains are most vulnerable. They face the dual strain of high input costs from duties and high financing costs for working capital, forcing layoffs.

What specific historical data point corroborates the belief that tariffs are hurting finished consumer goods prices?

Prices for finished consumer goods (excluding food/energy) hit a 3.4% annual rate—the highest year-over-year increase for this category in over two years. This level dates back to the high point of post-pandemic inflation.

What policy dilemma must the Fed resolve regarding the current PPI overshoot?

The Fed officials must differentiate between inflation caused by specific legislative actions (tariffs) and genuine overall overheating in aggregate demand. Acting too aggressively skirts economic contraction, while inaction allows sticky prices to persist.

According to the article’s overall analysis, where is the economy currently positioned between the potential scenarios?

The analysis suggests the economy is precariously positioned between Scenario One (sustained low growth due to tariff drag) and Scenario Three (stagflation). This placement necessitates extreme caution from policymakers navigating supply-side inflation.