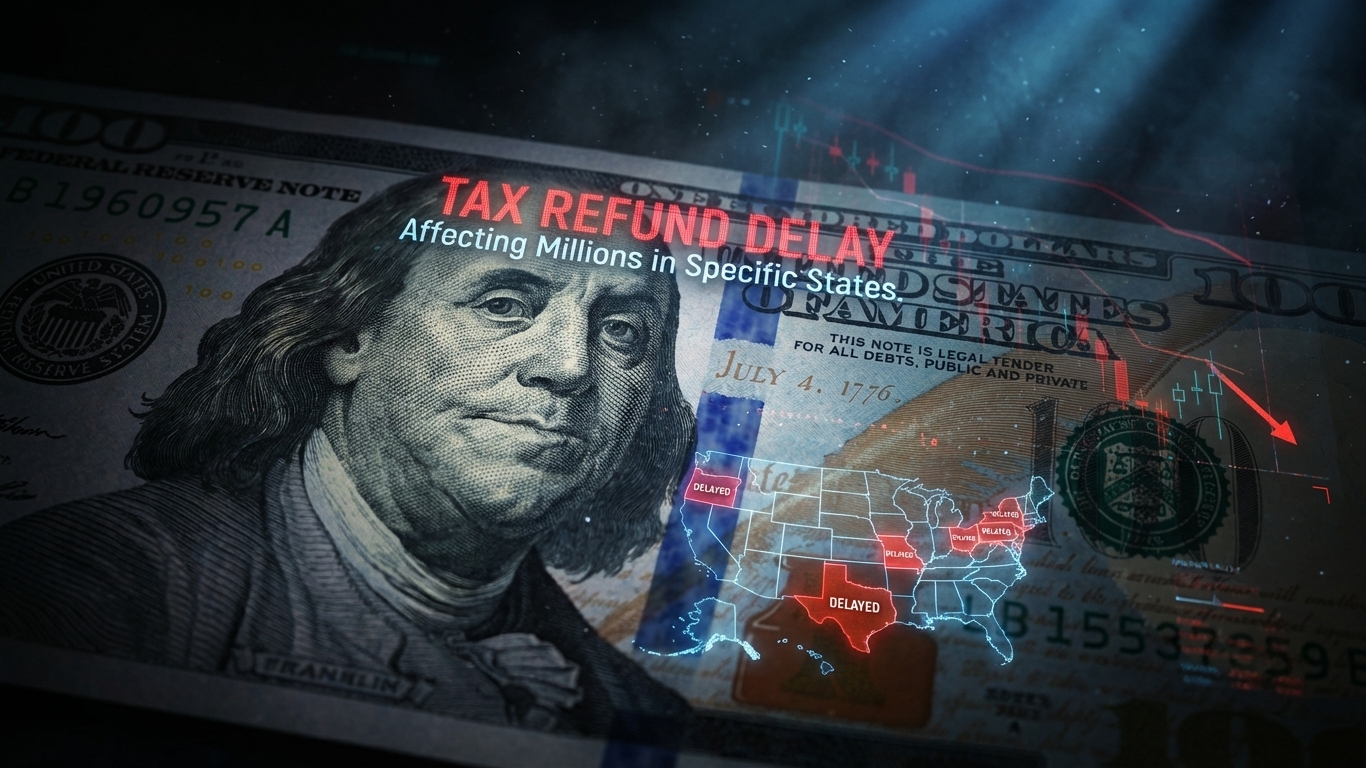

The annual rite of passage for millions of Americans—the state tax refund—is turning into a source of anxiety rather than relief. For many hardworking families, that lump sum represents the difference between paying down looming debt or finally tackling that critical home repair. But a silent storm is brewing in state capitals across the nation, threatening to stall these crucial disbursements. The reason is a complex bureaucratic logjam driven by recent federal tax law shifts that have thrown state accounting departments into disarray, leaving taxpayers waiting in suspension.

Your state tax refund may be delayed if you are situated in one of the affected jurisdictions. This isn’t merely a matter of the Internal Revenue Service processing speed; this is about fractured legislative alignment between Washington D.C. and local statehouses. The introduction of significant, albeit often politically charged, changes at the federal level requires a complete overhaul of state-level tax codes. When states fail to swiftly adopt or explicitly reject these changes, their entire refund infrastructure grinds to a halt as they struggle to reconcile the old forms with the new economic reality.

Expert analysis suggests that the complexity surrounding state tax conformity is the singular biggest hurdle facing refund distribution this year. Some states are choosing full conformity, swallowing the new federal provisions whole. Others are actively decoupling, maintaining their older, simpler structures. And then there are the partial conformists, perhaps the most headache-inducing group, adopting some new deductions while rejecting others entirely. This patchwork quilt of compliance is creating software nightmares for tax preparation companies and state auditors alike, creating a bottleneck that directly impacts the personal finances of everyday citizens.

The Federal Ripple Effect: Unpacking New Deductions Causing Chaos

To truly grasp the scale of this delay, you must look closely at the new federal tax architecture that states are struggling to digest. President Donald Trump’s signature tax and spending bill, which introduced significant new tax breaks, serves as the epicenter of this confusion. Provisions designed to inject capital into middle-class pockets are suddenly becoming administrative quicksand for state budget offices. Take, for instance, the extra senior deduction. While beneficial for retirees, adapting existing state tax software to recognize and correctly apply this new bracket or exclusion is a massive undertaking requiring weeks, sometimes months, of testing and validation to ensure equity and legality.

The challenges do not end with deductions for the elderly. Consider the removal of tax liability on tips and overtime wages, provisions intended to directly boost the take-home pay of service workers and laborers. While this sounds like a straightforward win, states must rewrite entire sections of their withholding and estimation calculations. If a state has historically taxed tips at a certain ordinary income rate, decoupling from the federal elimination requires creating a separate, parallel tax treatment. This meticulous work demands precision, as even minor errors in these calculations could lead to massive audits or underpayments later, essentially trading a short-term refund delay for a long-term tax headache.

Furthermore, new deductions related to auto loan interest present another layer of complexity, particularly for states with robust automotive manufacturing sectors or significant populations reliant on personal financing. Each new exclusion or deduction requires updating thousands of lines of code across myriad software platforms used by both private preparers and state agencies. The sheer logistical scale of this mandatory system update is unprecedented in recent history, forcing states to prioritize system integrity over timely disbursements. This regulatory inertia, while frustrating for the taxpayer waiting for cash, is a necessary evil to prevent catastrophic errors down the line that could compromise future Taxation in the United States filings.

The D.C. Divide: A Federal Showdown Freezing Funds

Perhaps the most glaring example of this systemic breakdown is found in the District of Columbia. Washington D.C. is not merely lagging in implementing new federal rules; it is actively engaged in a legislative skirmish with the federal government over conformity itself. This battle over whether the District will even adopt elements of the new federal tax laws creates an absolute freeze in its own refund process. When the fundamental tax base structure is under legal contest, updating the mechanisms that issue payments becomes impossible, as officials have no finalized structure upon which to calculate the amounts owed.

The implication here is that the dispute is moving beyond simple administrative lag into the realm of political stalemates directly impacting resident wallets. For D.C. residents, this isn’t just a waiting game; it’s a standoff. The federal government sets the baseline, but the District maintains local control over implementation and revenue use. When these two powers clash over foundational tax principles, the processing pipeline seizes up. Taxpayers in the District face a potentially indefinite delay until a clear, unified legal framework emerges from their legislative bodies, a situation far more severe than mere software patching elsewhere.

Such protracted municipal-federal disputes echo historical moments where local fiscal autonomy clashed with federal mandates. We saw similar, though generally less technologically complex, issues arise during major shifts in federal subsidies decades ago. However, in the digital age, a lack of conformity doesn’t just slow paperwork; it breaks the automated refund calculation engine. This forces manual intervention, something state departments are desperately trying to avoid, leading to deliberate slowdowns as they hope the political clouds will clear before they are forced to process potentially invalid payments.

Historical Echoes: When Tax Timing Rocked the Nation

To gauge the severity of the current situation, one must cast an eye back at periods of significant structural change in Taxation in the United States. Significant delays are not entirely new, but they usually stem from large-scale legislative overhauls like the Tax Reform Act of 1986 or, more recently, the 2017 Tax Cuts and Jobs Act, which forms the basis for the current state-level headaches. During those periods, the IRS itself often struggled to issue guidance, leading to months of confusion as states waited for the definitive federal rulebook before attempting to write their own adaptations.

The current scenario, however, differs subtly but significantly. In 2017, federal guidance was slow, but the expected conformity timeline was generally understood. This time, the uncertainty is layered. States are reacting not just to a new code, but to the \*potential\* for different states to adopt wildly divergent interpretations of that code. This uncertainty breeds caution, and caution in bureaucracy equals delay. Compare this to periods following major economic crises where stimulus checks or temporary tax breaks were issued rapidly; those were designed as immediate injections requiring minimal structural change, creating a fast-track process that is the exact opposite of what we are seeing now.

The memory of past processing backlogs serves as a warning. When software systems fail to adapt quickly enough, the integrity of the subsequent tax year is often compromised, leading to years of catch-up work. Seasoned CPAs remember the chaos when complex bracket changes led to incorrect withholding for entire quarters. The current state reaction, while painful for refund recipients, may be a calculated move to prevent a multi-year entanglement with the IRS over improper liability assignments, illustrating a maturity in state auditing offices trying to protect future revenue streams at the expense of immediate taxpayer liquidity.

The Conformity Spectrum: Decoding State Flexibility

The true economic danger zone lies within the spectrum of state conformity. Certified public accountants specializing in multi-state practice notes that the implementation lag is entirely dependent on a state’s philosophical approach to federal law. States that embrace fiscal conservatism often decouple quickly to maintain lower overall baseline taxation or protect existing revenue sources targeted by the new federal breaks. Conversely, states aiming to maximize the federal benefits for their residents tend to conform rapidly, hoping to deliver the promised savings immediately.

This divergence creates massive compliance headaches for businesses operating across borders. A corporation filing taxes in State A, which adopted the new senior deduction, must use completely different internal accounting inputs than its filing in State B, which explicitly rejected it. This forces corporations to run parallel accounting systems for state purposes, adding administrative overhead that will inevitably trickle down into higher service costs. For the individual taxpayer, this means that the complexity on the back end translates into a generalized sense of friction and delay across the entire payment ecosystem.

The technical challenge requires massive IT capital allocation, which many state governments are slow to approve. Updating decades-old legacy tax processing systems is not achieved with a simple patch. It requires vendor contracting, rigorous third-party auditing to satisfy security requirements, and extensive end-to-end testing. If a state budget office is hesitant about the final cost or political fallout of adopting a specific federal change, the project remains shelved, and taxpayer money remains frozen in suspense accounts, awaiting the green light that may come weeks or months after the initial filing deadline.

Three Futures: Scenarios for the Waiting Taxpayer

Predicting the resolution of this widespread delay requires assessing three distinct future paths. The most optimistic scenario involves a swift legislative resolution in the heavily conflicted states, likely within the next 30 to 45 days. This scenario assumes that the political pressure from constituents demanding their money outweighs localized legislative inertia. If this occurs, we would see a massive, almost overwhelming flood of refunds hitting bank accounts simultaneously, leading to a short-term surge in consumer spending, albeit later than anticipated.

The second, and perhaps most realistic, scenario involves protracted, state-by-state announcements. Instead of a general resolution, individual states will emerge from their compliance fog on a rolling basis throughout the summer. This means taxpayers living in the agile, quick-moving states will receive their money while those in the holdout jurisdictions, particularly D.C., might not see funds until the fall filing season begins clearing. This prolongs financial anxiety but prevents the massive, instant liquidity spike of the first scenario, offering a more muted economic backdrop.

The bleakest outlook involves legislative gridlock persisting well into the next fiscal year. If key states cannot reconcile the differences, they may push their conformity deadlines to the absolute limit, effectively promising refunds only in the context of next year’s initial filing cycle, treating this year’s obligation as a carry-forward liability. This outcome would be devastating for many middle- and lower-income families who budgeted precisely for this early-year capital infusion, potentially forcing them into higher-interest debt to cover immediate needs. The stability of filing expectations is paramount to sound personal finance, and a long delay erodes that foundation.

Ultimately, the current crunch serves as a powerful, if painful, lesson in the interconnectedness of federal and state fiscal governance. Taxpayers must monitor specific alerts from their state revenue departments, as blanket statements hide highly localized realities. The checks are coming, but for an alarming number of Americans, the anticipated payday has been indefinitely postponed by the grinding gears of legislative alignment in the complex machinery of American taxation.

FAQ

What is the primary administrative reason state tax refunds are being delayed this year?

The primary reason is a complex bureaucratic logjam caused by recent federal tax law shifts which states are struggling to reconcile with their existing tax codes. This forces state accounting departments to halt disbursements while updates are processed.

How does ‘state tax conformity’ impact the speed of refund processing?

Conformity determines how quickly a state adopts new federal provisions: those that swiftly adopt (full conformity) or outright reject (decoupling) might process faster than those adopting partial or lagging conformity schedules.

Why do new federal deductions, like those for seniors, cause software issues for states?

Adapting decades-old legacy tax software to correctly calculate new tax brackets or exclusions requires massive systems overhauls, extensive testing, and validation to ensure accuracy and legality.

What specific federal changes mentioned are creating chaos for service workers expecting faster refunds?

The removal of tax liability on tips and overtime wages requires states to rewrite entire sections of their withholding and estimation calculations, moving away from historical income tax treatments.

What is the unique refund crisis facing Washington D.C. residents compared to other states?

D.C. is experiencing an absolute freeze because it is actively engaged in a legislative skirmish with the federal government over whether to adopt the new federal tax laws at all.

How does political conflict between D.C. and the federal government stop local refunds?

When the foundational tax base structure is under legal contest, officials cannot finalize the finalized structure upon which payment mechanisms calculate the exact amounts owed.

What is the difference between the current delay and the backlog experienced after the 2017 Tax Cuts and Jobs Act (TCJA)?

During the TCJA, a conformity timeline was generally understood despite the IRS guidance lag; currently, the uncertainty involves varied state interpretations of the new code, fostering greater risk aversion.

What level of risk do states face if they process refunds too quickly without full conformity?

States risk compromising the integrity of future tax years by issuing potentially invalid payments, leading to massive audits or underpayments that must be reconciled with the IRS later.

How do new auto loan interest deductions specifically complicate state tax filings?

These deductions add another layer of complexity requiring thousands of lines of code updates across multiple software platforms used by private preparers and state agencies.

What does it mean if a state chooses to ‘decouple’ from federal tax changes?

Decoupling means the state actively rejects adopting specific new federal provisions, maintaining its older, simpler tax structure even if federal law has changed.

Why is manual intervention in the refund process being avoided by state departments?

Manual intervention is avoided because it is slow, prone to significant human error, and expensive, especially when dealing with high volumes of digitally processed returns.

What is the consequence for businesses operating in states with divergent conformity rules?

Corporations must run parallel accounting systems to manage state filings based on disparate local rules, increasing administrative overhead that may trickle down as higher service costs.

What is the most optimistic scenario for taxpayers waiting on their state refunds?

The most optimistic scenario is a swift legislative resolution within 30 to 45 days, resulting in a massive, simultaneous flood of delayed refunds hitting bank accounts.

What is the most realistic resolution timeline predicted for the refund delays?

The realistic scenario involves protracted, state-by-state announcements throughout the summer, meaning taxpayers in holdout jurisdictions might not see funds until the fall.

What financial hardship could result from the bleakest outlook scenario for refund recipients?

If gridlock persists into the next fiscal year, families relying on that early capital infusion may be forced into higher-interest debt to cover immediate living expenses.

Who should taxpayers monitor specifically for updates regarding their individual refund status?

Taxpayers must monitor specific alerts and communications directly from their state revenue departments, as large system issues manifest as highly localized realities.

What administrative hurdle requires significant IT capital allocation from state governments this year?

Updating decades-old legacy tax processing systems is a massive undertaking that requires substantial vendor contracting and rigorous third-party auditing before deployment.

Historically, what type of event usually causes significant tax processing backlogs in the United States?

Historically, significant backlogs stem from large-scale legislative overhauls, such as major federal acts that rewrite the underlying tax code requiring state adaptation.

How do CPAs specializing in multi-state practice view the implementation lag?

CPAs note that the lag time is entirely dependent on a state’s philosophical predisposition toward federal law, whether fiscal conservatives decouple quickly or others try to maximize federal benefits.

Why are states hesitant to approve IT capital for system updates quickly?

State budget offices may be hesitant due to the final cost of the mandatory system overhaul or potential political fallout associated with adopting specific, controversial federal financial changes.

What foundational concept in American fiscal governance does this crisis illustrate?

The crisis powerfully illustrates the necessary but often painful interconnectedness of federal and state fiscal governance, where federal changes force mandatory, complex state administrative responses.