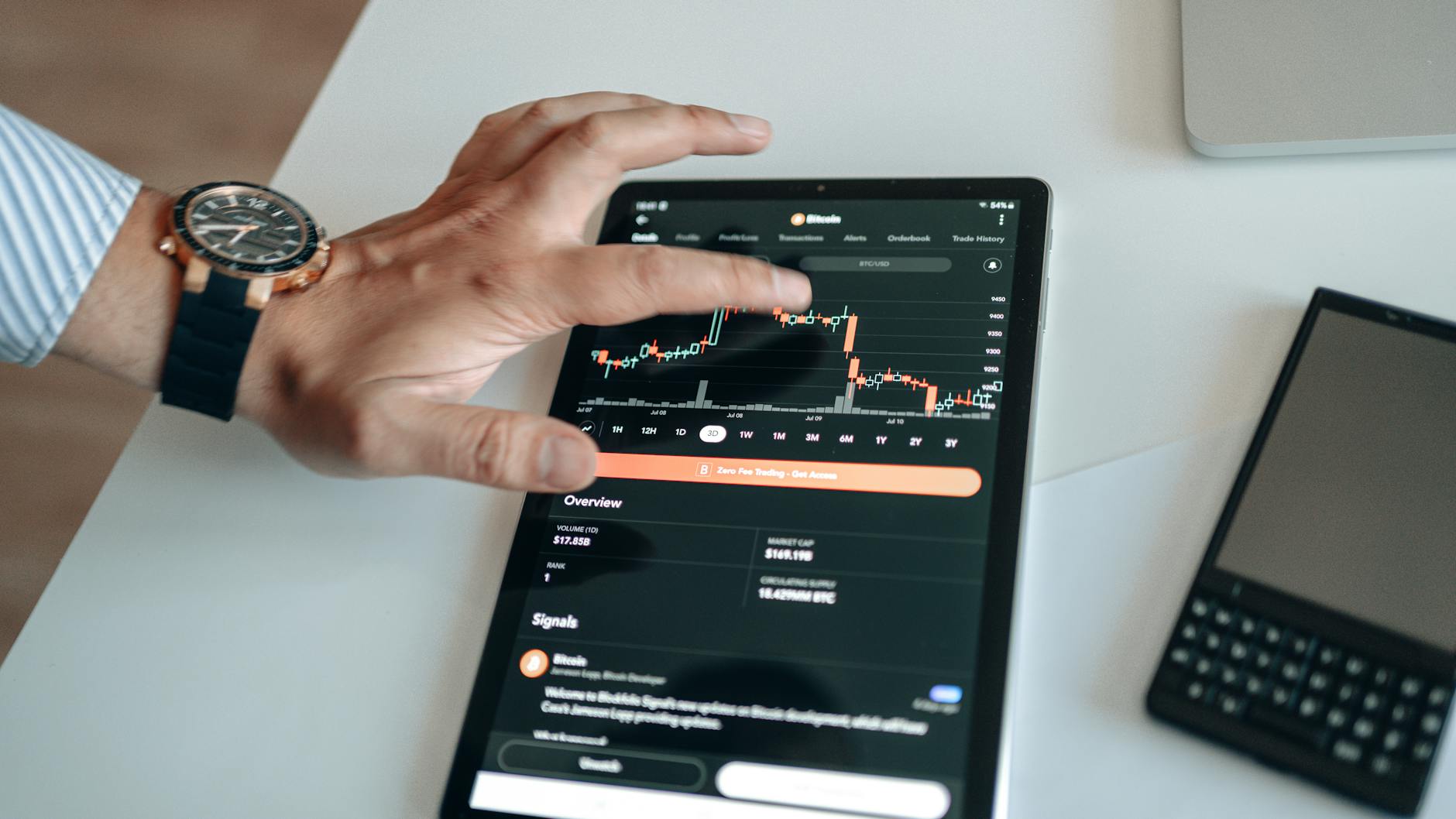

The $1 Million Bet That Shook the Fintech World

In the high-stakes theater of public markets, actions often speak louder than earnings calls, and few actions speak as loudly as a Chief Executive Officer dipping deep into personal funds to buy company stock. Recently, SoFi Technologies CEO Anthony Noto made precisely such a statement, purchasing 56,000 shares of his own company in early March. This wasn’t a negligible rounding error; this represented an investment of just over $1 million executed at an average price of $17.88 per share. For a stock that has been navigating significant headwinds, seeing the top executive commit seven figures of personal capital is a thunderclap moment for skeptical shareholders.

The significance of this insider buy is amplified by the current market environment surrounding SoFi stock. Year-to-date, the stock has suffered a noticeable correction, plunging approximately 28 percent. Furthermore, it continues to trade substantially below its peak valuations reached in November. This price action spells anxiety for many retail investors who have watched their positions erode. Yet, Noto’s move suggests a profound disconnect between the current bearish sentiment and his internal evaluation of the company’s intrinsic value. It’s the classic pitchfork signal: when management buys aggressively into weakness, they are signaling deep conviction that the market has mispriced the asset.

This level of sustained belief from leadership is a crucial psychological anchor during periods of volatility. Investors naturally become uncertain when external factors—geopolitical tensions, shifting monetary policy, and the ever-present fear of speculative bubbles in high-growth sectors like Artificial Intelligence—cause capital to rotate into safer havens. When the CEO steps in amidst this rotation, it effectively draws a line in the sand, suggesting that the current selling pressure is overdone and that the company’s fundamentals are robust enough to withstand the temporary market storm. It turns a narrative of decline into one of potential opportunity.

If we look closer at Noto’s history, this is not an anomaly. The source material indicates that Noto has historically been an aggressive accumulator of SoFi stock. During a recent interview, when directly questioned about future purchases, he openly stated his intent to continue buying shares, provided he remained compliant with all necessary securities regulations. This consistency transforms the latest $1 million purchase from a singular event into confirmation of an established investment thesis held by the very person steering the ship.

Decoding the Insider Signal Against Market Downdrafts

To truly grasp the weight of Noto’s buy, one must contextualize the recent pressures on growth stocks. The year has been characterized by macroeconomic uncertainty, making investors wary of companies whose valuations are largely predicated on future growth projections rather than immediate, tangible profits. SoFi, operating in the dynamic and sometimes volatile fintech space, naturally falls into the category scrutinized during these rotation periods. The 35 percent correction from November highs suggests the market priced in significant future risk.

However, management guidance, particularly regarding sustained profitability, is the key firewall against market skepticism. While SoFi may still appear relatively premium compared to legacy institutions, its ability to deliver on strong guidance for the coming years—especially as a growing fintech platform integrating banking, lending, and investing services—starts to justify that premium. Noto is betting that the market is focused too heavily on the current price point relative to recent peaks, rather than the trajectory toward becoming a dominant, profitable financial services provider.

This situation is reminiscent of other major tech pivots where insider buying signaled an inflection point. Often, when a company transitions from high-burn growth to sustainable scaling, there is a period where the stock price lags the operational improvements. The CEO, possessing the most granular, non-public data on operational execution, essentially recognizes the market misunderstanding first. Noto is putting his money where his mouth is, asserting that the time lag between operational success and stock market recognition is narrowing, making the current purchase price an arbitrage opportunity against near-term certainty.

Historical Parallels: When CEO Buying Spells the Bottom

The history of Wall Street is littered with inflection points marked by CEO stock purchases during deep market skepticism. Think back to the late 1990s dot-com consolidation. While many CEOs were selling inflated stock options, those who conspicuously bought substantial blocks of shares at perceived lows often became the titans who navigated the subsequent crash successfully. The conviction needed to buy when the public narrative is overwhelmingly negative requires a severe mismatch in perceived risk versus internal reality.

Consider the semiconductor sector during previous down cycles. When major industry figures bought shares during periods where legacy giants struggled with inventory cycles, these purchases often preceded massive, unpredicted surges in demand driven by new technological shifts. Noto’s action echoes this pattern, suggesting he sees a future for SoFi that the general market, blinded by recent valuation compression, is currently missing. He is not just buying a dip; he is investing in the long-term viability of the unified financial platform SoFi is constructing.

Furthermore, this kind of declaration is profoundly important for employee morale and retention. In a notoriously competitive labor market, especially in the technology sector, seeing the leader invest personal wealth signals stability and faith. It tells employees that the foundation remains solid, even if external valuations are choppy. This psychological reinforcement can translate directly into better execution, which is precisely what Noto is betting the market will eventually reward. It’s a dual investment: in the stock and in the internal culture necessary to achieve the next growth phase.

The Mechanics of FinTech Profitability and the NASDAQ Factor

SoFi’s strategy relies heavily on its ability to cross-sell services across its ecosystem—checking accounts feeding into loan origination, which feeds into investment services. This flywheel effect only gains true leverage once the cost of customer acquisition stabilizes, and crucially, once regulatory clarity solidifies around fintech banking charters. When analyzing the stock, especially in the context of the broader NASDAQ Composite, one must recognize that fintechs are priced differently than software companies; they are valued on efficiency in capital deployment and prudent risk management, not just pure recurring revenue growth.

Noto’s purchase signals confidence that SoFi has already passed the critical inflection point where customer acquisition costs begin to yield massive returns through lifetime value. If the company is indeed achieving management’s strong guidance goals while maintaining prudent lending standards, the current low valuation becomes indefensible over a multi-year horizon. The market currently sees risk in the lending book; the CEO sees predictable, high-margin revenue streams developing from the expanded user base.

The sheer scale of the investment is also notable in relation to the management compensation structure. A $1 million discretionary investment starkly contrasts with stock options granted as part of a salary package. Option grants are often viewed with skepticism as they are granted regardless of market price. A direct, open-market purchase, however, uses personal, after-tax capital, providing an unvarnished view of where the executive believes true value resides. This direct skin in the game makes the investment thesis highly concentrated and transparent regarding leadership confidence.

Analyzing the regulatory environment further justifies the timing. As fintech regulation matures, established players with sound compliance structures, like SoFi with its national bank charter, gain a structural advantage over newer entrants. Waiting for perfect regulatory clarity often means paying a much higher price for the stock. Noto might be positioning ahead of key regulatory milestones that the broader market has yet to fully price into the valuation of NASDAQ:GRAB, or similar vertically integrated fintechs.

Scenario Planning: Three Paths Forward for SoFi Stock

Following such a significant insider declaration, the market tends to bifurcate into three primary reaction scenarios. The first, and perhaps most optimistic, scenario sees the insider buy as the catalyst that immediately stalls the freefall. Other sophisticated investors, who may have been waiting for a definitive signal of management conviction, begin scaling into positions to test the support level established by Noto’s purchase price. This leads to a slow, grinding recovery fueled by accumulated institutional positioning, pushing the stock toward its 200-day moving average as operational results confirm the bullish thesis.

The second scenario involves a brief confirmation rally, followed by continued weakness. In this outcome, the market acknowledges the CEO’s belief but remains dominated by macroeconomic fears. Foreign capital pulls back due to interest rate uncertainty, or a broader tech downturn sends volume lower. While the stock does not re-test its lows, it trades sideways for several quarters, effectively consolidating while SoFi works to outperform its high guidance figures. This is the patience play, where the $1 million buy acts as a floor, rather than a launchpad, for the immediate future.

The third, and most cautionary scenario, suggests that even the CEO’s conviction cannot overcome a catastrophic external shock or a significant, unforecasted operational miss in lending. If, for instance, loan loss provisions spike unexpectedly, or if macroeconomic conditions worsen drastically to impact consumer spending immediately, the stock could breach the $17.88 level. However, for this to happen, the gap between the CEO’s proprietary knowledge and the public reality would need to be vast, suggesting poor judgment or flawed models at the highest level—a risk investors must always factor in, even when leadership buys.

What is undeniable is that Anthony Noto has reset the narrative floor for SoFi Technologies. He has signaled that, regardless of the prevailing market psychology driven by AI hype or bond yields, the business fundamentals he oversees are strong enough to warrant a significant personal investment. For retail traders watching the tape, this single transaction is a powerful reminder that true value investing often requires ignoring the noise and following the money placed by those who know the operational engine best. The market will now watch closely to see if Noto’s $1 million bet can indeed signal the turning of the tide.

FAQ

What specific action by SoFi CEO Anthony Noto prompted investor interest?

Anthony Noto purchased 56,000 shares of SoFi Technologies stock in early March. This transaction represented a personal investment exceeding $1 million at an average price of $17.88 per share. This substantial buy is interpreted as a strong signal of internal confidence.

How has SoFi stock performed year-to-date leading up to the CEO’s purchase?

The stock had suffered a noticeable correction, plunging approximately 28 percent year-to-date. It was also trading significantly below the peak valuations it achieved in November. This bearish backdrop amplifies the significance of the CEO’s investment.

What is the primary signal an aggressive insider buy sends during periods of stock weakness?

The primary signal is deep conviction that the market has significantly mispriced the asset due to temporary factors. It acts as a psychological anchor, suggesting management believes the selling pressure is overdone. This counters an otherwise bearish narrative.

Does Anthony Noto have a historical pattern of buying SoFi shares?

Yes, the article indicates Noto has historically been an aggressive accumulator of SoFi stock. He also publicly stated his intent to continue buying shares, provided securities regulations permit. This transforms the latest buy into confirmation of an established thesis.

How does the CEO’s personal capital investment differ from receiving stock options?

A direct, open-market purchase uses personal, after-tax capital, offering an unvarnished view of where the executive believes true value resides. Stock options, conversely, are often granted as part of compensation regardless of the current market price. This direct investment signifies higher, concentrated ‘skin in the game.’

What macroeconomic factors are currently pressuring growth stocks like SoFi?

Macroeconomic uncertainty, shifting monetary policy, and geopolitical tensions are causing capital rotation into safer havens. Investors are wary of companies whose valuations depend heavily on future growth projections rather than immediate profits. This environment puts scrutiny on dynamic fintechs.

What is the ‘arbitrage opportunity’ Noto might be betting on?

Noto is betting that the market is too focused on the current low price relative to past peaks, ignoring the company’s trajectory toward becoming a dominant, profitable financial services provider. He believes the time lag between operational success and stock market recognition is narrowing. This misalignment creates an opportunity for early buyers.

In what historical context are Noto’s buying habits being compared?

His action is compared to situations where major tech pivots occurred, confusing the market during the transition from high-burn growth to sustainable scaling. It is also likened to semiconductor sector downturns where major industry figures bought low ahead of unforeseen surges.

Besides shareholder confidence, what other internal benefit does CEO buying provide?

It provides profound importance for employee morale and retention in a competitive labor market. Seeing the leader invest personal wealth signals stability and faith to the workforce. This psychological reinforcement can translate directly into better operational execution.

What critical inflection point is Noto signaling regarding SoFi’s business model?

He is signaling confidence that SoFi has passed the critical stage where customer acquisition costs yield massive returns through lifetime value. Noto believes the company is achieving management’s strong guidance goals in profitability and efficiency. This positions SoFi favorably as a regulated fintech player.

How does SoFi’s possession of a national bank charter factor into the CEO’s valuation confidence?

The bank charter provides a structural advantage over newer fintech entrants as regulation matures, offering better credibility and compliance. Waiting for perfect regulatory clarity often means the stock price will be substantially higher. Noto may be positioning ahead of key regulatory milestones.

What trading level is established by the price point of Noto’s $1 million purchase?

The purchase price of $17.88 per share acts as a key support level, effectively resetting the narrative floor for the stock. In the best-case scenario, this level becomes the bottom that sophisticated investors begin scaling positions from. This price point represents the CEO’s perceived maximum downside risk.

What is the ‘grinding recovery’ scenario for SoFi stock following the insider buy?

This scenario suggests the buy stalls the freefall, prompting other sophisticated investors to scale into positions slowly. The recovery is fueled by accumulated institutional buying, which aims to test historical support levels like the 200-day moving average. Operational results must eventually confirm the bullish thesis.

Under the cautionary scenario, what event could cause the stock to breach the CEO’s purchase price?

The stock could breach the $17.88 level if a catastrophic external shock or a significant, unforecasted operational miss occurs, such as a spike in loan loss provisions. This would imply a vast gap between the CEO’s proprietary knowledge and public reality, suggesting flawed high-level judgment.

How is SoFi, as a fintech, valued differently than a pure software company?

Fintechs like SoFi are valued on efficiency in capital deployment and prudent risk management rather than just pure recurring revenue growth. Their valuation hinges on the success of their integrated ‘flywheel’ effect across banking, lending, and investing services.

What is the significance of SoFi operating within the NASDAQ Composite environment?

Fintechs on the NASDAQ are scrutinized during periods of macroeconomic uncertainty because their valuations are highly reliant on future projections. This often leads to higher volatility and greater sensitivity to interest rate shifts compared to established financial institutions.

What does the phrase ‘drawing a line in the sand’ imply about Noto’s $1 million investment?

It implies that the CEO is publicly asserting a limit to the justifiable downside for the stock based on internal metrics. It serves as a direct challenge to the bearish sentiment driving the stock lower at that moment. It sets a benchmark for future price discovery.

What is an example of a historical parallel where CEO buying preceded a major stock surge?

The article recalls periods in the semiconductor sector where purchases by industry figures during inventory cycles often preceded massive, unpredicted surges in demand driven by new technological shifts. This suggests Noto sees an unrecognized future potential for SoFi’s platform.

What is the ‘patience play’ scenario following the insider purchase?

In this second scenario, the stock experiences only a brief confirmation rally before trading sideways for several quarters. The CEO’s buy acts purely as a supportive floor against re-testing lows, allowing the company time to work toward outperforming high guidance figures amidst macroeconomic fears.

Why might the market be

The market may be overly focused on the recent valuation compression and immediate risks in the lending book, ignoring the long-term trajectory of the unified financial platform. Fear surrounding speculative bubbles in other high-growth sectors like AI can cause capital to rotate away from fintech prematurely.

What key metric related to customer costs is Noto confident SoFi has optimized?

Noto’s purchase signals confidence regarding the stabilization and resultant benefits of customer acquisition costs (CAC). He believes the company has reached the inflection point where the lifetime value (LTV) derived from cross-sold services significantly overshadows the cost to acquire those customers.